For the last nine years, the Alternative Minimum Tax (AMT) has receded from view for many high-income households. The 2017 Tax Cuts and Jobs Act (TCJA) raised exemption amounts and pushed phaseout thresholds high enough that AMT became a concern primarily for those with very specific tax profiles. Beginning in 2026, that changes.

While the One Big Beautiful Bill Act (OBBBA) permanently extends the higher AMT exemption amounts introduced under the TCJA, it also significantly alters how quickly those exemptions disappear. The combination meaningfully expands the population exposed to AMT and changes how the tax behaves for affected households. For many high earners, AMT is once again a meaningful planning consideration.

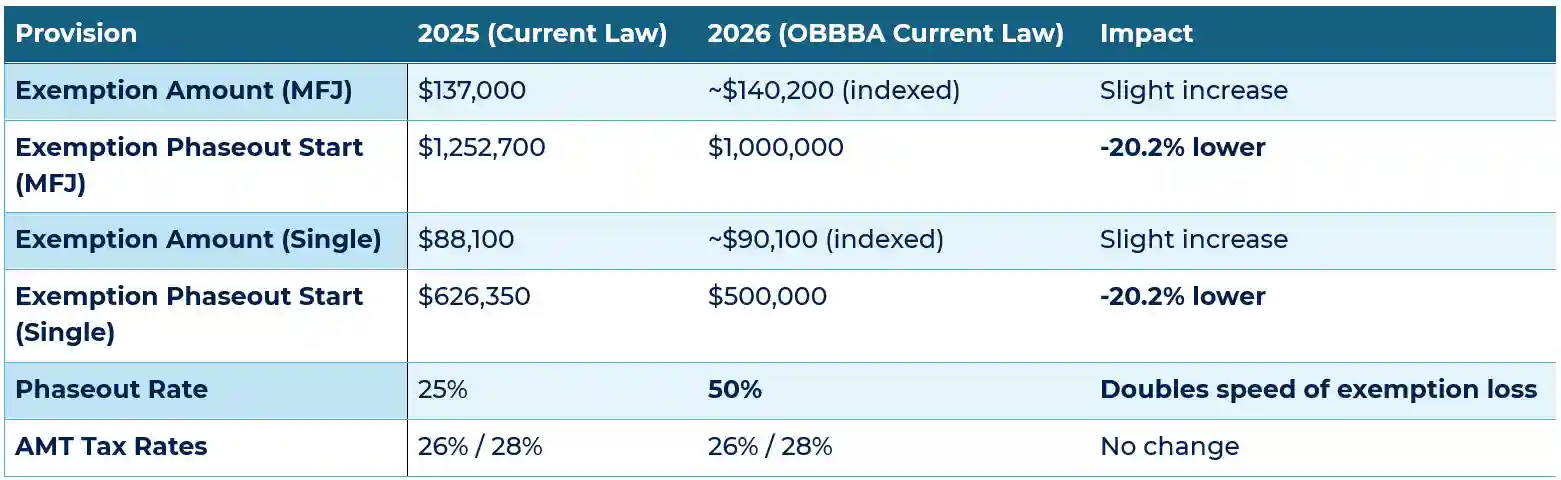

Core Structural Changes Under OBBBA

While headline attention has focused on the permanence and size of the AMT exemption, the more consequential changes occur in the phaseout mechanics.1

The practical effect is straightforward. Once income crosses the phaseout threshold, the AMT exemption is lost twice as quickly as before.

Why Phaseout Mechanics Matter More Than the Exemption Amount

Under prior law, the AMT exemption phased out gradually. Households could often absorb modest increases in income without fully losing the exemption. Under OBBBA, that cushion largely disappears. For 2026, a married couple’s AMT exemption is fully phased out at approximately $1.28 million of AMT income, compared to roughly $1.8 million under 2025 rules. This compresses the AMT exposure window and increases the likelihood that ordinary planning events trigger AMT liability.2 The result is not necessarily a higher permanent tax burden, but a sharper sensitivity to income timing and tax aware planning.

Taxpayer Profiles Most Likely to Be Affected

- Married households earning $750,000 to $1.5 million: This income range represents the center of new AMT exposure. State and local taxes, property taxes, and one or two AMT preference items are often sufficient to push these households into the phaseout zone.

- Executives exercising incentive stock options: ISO exercises remain a significant AMT preference item. Under the accelerated phaseout, the same exercise that produced manageable AMT exposure in 2025 can generate materially higher liability in 2026.

- High-tax state residents: SALT deductions continue to be fully disallowed for AMT purposes. While the SALT cap increases for regular tax in 2026, that relief does not apply under AMT, amplifying exemption loss once phaseout begins.

- Investors holding private activity bonds: Interest that is tax-exempt for regular tax remains taxable for AMT. Lower thresholds mean this income now affects AMT exposure earlier and more forcefully.

- Households with uneven income timing: Large bonuses, deferred compensation payouts, liquidity events, or concentrated capital gains in a single year create disproportionate AMT effects under the new phaseout structure.

In practical terms, the AMT phaseout creates a hidden tax increase. Even though the stated AMT rates stay at 26% and 28%, losing the exemption as income rises effectively pushes the tax rate higher. For many households, that blended outcome results in an effective marginal tax rate in the low-to-mid 30% range during the phaseout. A simple example helps illustrate why:

- Assume a married household earns $1,000,000 in 2026, placing them right at the start of the AMT phaseout. They then recognize an additional $100,000 from a bonus, stock sale, or ISO exercise, bringing total income to $1,100,000.

- Under the 2026 AMT rules, that additional $100,000 causes a $50,000 reduction in the AMT exemption due to the 50% phaseout rate. The AMT exemption is approximately $140,200 at $1,000,000 of income. After the phaseout, it falls to $90,200, meaning an additional $50,000 of income becomes subject to AMT at 28%, resulting in $14,000 of incremental tax.

- Putting the pieces together, that extra $100,000 of income ends up being very expensive in the AMT phaseout range. If it’s long‑term capital gain, the effective federal tax is roughly $34,000 (about 34%). If it’s ordinary income or an ISO bargain element, the effective federal tax is closer to $42,000 (about 42%).

- This effect is most pronounced when capital gains or ISO exercises are added on top of already high income, since those items can push income deeper into the phaseout range very quickly.

Planning Implications Going Forward

- Income timing becomes more important: Accelerating income into 2025 or deferring income beyond peak AMT years can materially reduce total tax paid across multiple years. This applies to bonuses, ISO exercises, and capital gain realization.

- ISO strategy requires closer modeling: Spreading exercises over multiple years or considering disqualifying dispositions may be preferable once the exemption phaseout is triggered, particularly when AMT credits are unlikely to be recovered efficiently.

- Capital gains planning deserves coordination: Gains realized in years where AMT exemption is already partially or fully phased out can carry higher effective tax costs than anticipated.

- Charitable planning still works, but timing matters: Charitable deductions are allowed for AMT purposes, but their value is maximized when contributions are timed outside heavy phaseout years. Donor advised funds remain a useful tool for separating deduction timing from gifting decisions.

- Multi-year projections are no longer optional: Single-year tax estimates frequently miss AMT dynamics. Three-year modeling often reveals planning opportunities that are invisible when each year is viewed in isolation.

When AMT Cannot Be Avoided

For some households, AMT exposure will be unavoidable given income levels and preference items. In those cases, the objective shifts from avoidance to management. That includes:

- Maximizing future use of AMT credits

- Avoiding decisions driven solely by tax considerations

- Recognizing that much AMT represents a timing issue rather than a permanent increase in lifetime tax burden

A Common Misconception

AMT is often described as a permanent penalty, but that characterization is incomplete. In many situations, AMT paid creates an AMT credit that can be used in future years to offset regular tax once regular tax exceeds AMT. This most commonly occurs when AMT is triggered by timing differences, such as incentive stock option exercises, accelerated income, or depreciation preferences that reverse over time.

That said, the AMT credit is not guaranteed to be recovered, and its usefulness depends heavily on future income, tax structure, and planning discipline. AMT credits are most likely to be recovered when:

- AMT is driven by ISO exercises where shares are later sold, eliminating the preference item

- Income normalizes in later years rather than remaining in the AMT phaseout range

- Regular tax in future years consistently exceeds AMT, allowing the credit to be used

In these cases, AMT often functions as a prepayment of tax, shifting liability forward rather than increasing lifetime tax paid. AMT credits are less reliable when:

- Income remains consistently high and continues to trigger AMT year after year

- AMT is driven by permanent preference items, such as state and local tax disallowance or private activity bond interest

- ISO shares decline in value before sale, leaving taxpayers with AMT paid on income that never materializes economically

- Credits accumulate faster than they can realistically be used, particularly late in a career or near retirement

In these situations, AMT behaves much more like a permanent cost. AMT should not be dismissed as temporary, nor should the credit be treated as a sure thing. Well-executed planning treats AMT credits as a potential offset, not an entitlement. The goal is to minimize unnecessary AMT, preserve flexibility, and avoid creating credits that may never be efficiently recovered.

The OBBBA changes both who encounters AMT and how quickly it becomes relevant. For high earners approaching seven-figure income, AMT planning is now a necessity once again. Households with variable income, equity compensation, or planned liquidity events need multi-year modeling that explicitly accounts for AMT phaseouts, income timing, and credit recoverability. If your income is likely to approach or exceed these thresholds in the coming years, now is the time to stress-test your plan. Coordinating ISO exercises, capital gains, charitable giving, and bonus timing before 2026 can materially reduce both tax friction and unpleasant surprises.

Given the complexity and evolving nature of AMT planning, it’s essential to evaluate your unique circumstances with expert guidance.

[1] Chart Source: https://www.thomsonreuters.com/en-us/posts/tax-and-accounting/obbba-faq/

[2] Source: https://www.doeren.com/viewpoint/irs-releases-2026-cost-of-living-adjustments-includes-amendments-from-obbba